Home » Articles » Reverse Mortgage for Loan: How It Can Help Senior Citizen?

Also, read this article in हिंदी, मराठी, తెలుగు, தமிழ், ગુજરાતી, and ಕನ್ನಡ

The Reverse Mortgage for Loan (RML) was Introduced in India in 2007 to boost the life of house-owning senior citizens. RML is a loan that allows them to fulfill their day-to-day expenses concerning food, medicine, and repair of the house. At an age when the majority of people don’t have a daily source of income in India, Reverse Mortgage for Loans is hope for them.

The minimum age of availing the RML is 60 years, regardless of the gender difference, and if a couple seeks a joint loan, then the age limit for the spouse is 55 years or above. The applicant must have his/her own purchased house as RML cannot be secured against the ancestor’s property. There are various factors on which banks and other financial institutions assess the worth of property, but it’s minimum residential life should not be less than 20 years.

A reverse mortgage for a loan is a unique kind of loan in which a borrower, usually a senior citizen only, can mortgage a property he or she already owns to a bank. The bank then pays a monthly amount to the borrower for the required tenure. Since it’s the bank paying the EMIs to the borrower during this loan, it’s called a reverse mortgage.

What is Reverse Mortgage for Loan?

A reverse mortgage for a loan is a good way for senior citizens to receive some funds if they’re in need of liquid cash and that they have a property in their name. Using their already owned property as a mortgage, the senior citizens can borrow money from a bank which is paid via monthly installments by the bank.

Eligibility of Reverse Mortgage for Loan?

The eligibility criteria for a reverse mortgage loan are:

- The borrower should be a citizen of India and should have a minimum age of 60 years.

- Married couples can jointly apply for the loan as long as one among them should be more than 60 years aged and therefore the other shouldn’t be below the age of 55.

- The borrower should be the owner of a self-acquired, inherited, or self-occupied residential property in India. The title of the property should clearly indicate the borrower’s ownership and it’s to be free from any liability, debt, or other obligations.

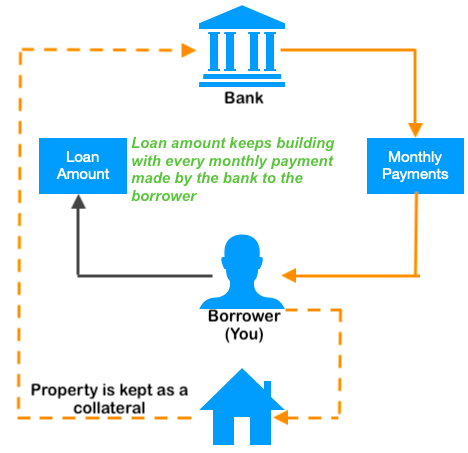

How Reverse Mortgage for Loan Work?

- Collateral: A borrower pledges the property as collateral to a bank or any financial organization which issues a loan to the borrower based on the valuation of the property.

- Monthly payments: After the property is pledged, the borrower is eligible to receive fixed periodic (monthly, quarterly, annually, or lump-sum) payments from the bank at a given rate of interest. Unlike a home loan, the borrower isn’t required to pay monthly payments towards interest and principal to the bank. The payments made by the lender over fixed loan tenure are referred to as ‘reverse EMI’.

- Property valuation: The pledged home’s price is decided by the lender based on the demand for the property, current rates, price fluctuations, and therefore the condition of the house. The lender re-values the pledged property every five years and increases the quantum of the loan if the valuation rises gradually.

- Occupation: Under the Reverse Mortgage Scheme, the owner (borrower) of the property is meant to stay within the pledged house as a primary residence during the tenure of the mortgage for a loan while he or she continues to receive periodic payments.

- Loan amount: The maximum monthly payment under this loan scheme is capped at Rs 50,000, and therefore the maximum lump-sum payment to be made is 50 percent of the entire loan amount with a cap of Rs 15 lakh. But the house owner house should keep paying all the taxes associated with the property, insure and maintain it as their primary residence. The loan amount increases gradually because the borrower receives payments and interest accumulates on the loan and home equity declines over time.

- Loan tenure: The maximum loan tenure is between 10 to fifteen years. Though, some financial institutions are offering till 20 years. After the loan tenure is over or the borrower lives longer than the tenure, the lender won’t make any longer payments, but the borrower can still stay within the house.

- Interest rates: Interest rates are charged on the payments borrower receives from the lender. Interest payments on the loan amount are deferred to the top of the loan tenure and aren’t paid out-of-pocket, up-front, or monthly. Basically, Reverse Mortgage defers all loan and interest repayment to the time when the loan amount matures.

Documents required for Reversed Mortgage Loan:

The following documents are required to avail of a reverse mortgage for loan:

- Permanent account number (PAN)

- Aadhaar card

- Registered will

- List of legal heirs

- Property details

A reverse mortgage is a perfect option for senior citizens who require a regular income to supplement their pension without depending upon anyone else. However, it should be seen as a final resort and not a routine kind of financing cash requirement for senior citizens.

Share this article on WhatsApp.

Also read: