How Stamp Duty and Registration Charges are Calculated on Property?

rimzim • September 29, 2020

Millions share the dream of buying a house in India. Soaring property prices across the country have elevated homeownership or home purchase to one of the most significant financial milestones. Soaring property values may paint a daunting picture. But with the support of a home loan, the dream of owning a home comes into focus. These financing options become a vital partner in the journey, providing the necessary boost to reach the goal. If you’re eligible for a home loan, your lender might approve a loan of 70%-85% of the property value. You need to arrange the remaining 40%-20%. But except for property cost, a buyer also must consider a bunch of additional expenses that accompany a property purchase. Two of the most important of them are stamp duty and registration charges.

If you’re going to purchase a property anytime soon, you must try and know as much about them as possible. This may assist you in making sure that you have adequate funds to manage these additional expenses. This will also fulfill your dream of buying a property.

What is Stamp Duty?

Every documented transaction is subject to a tax known as stamp duty. Stamp duty may include a conveyance deed, sale deed, power of attorney, etc. It is a tax that’s paid for acquiring any document or instrument that facilitates the creation, transfer, limiting, extending, extinguishing, or recording of any right or liability. Stamp duty started after the passing of the Indian Stamp Act in 1899. Once you pay stamp duty, these papers become legally valid and can hold up in court.

How is it calculated?

Stamp duty calculation relies on the worth of the property. Each Indian state has its own criteria supported by which it is calculated. it is generally paid on the idea of the circle rate that is determined by a government. Stamp duty also varies on the premise of the type of property i.e. residential or commercial, also as for urban and rural areas.

There are 3 ways within which you’ll pay stamp duty for the new property you’re close to owning. you’ll consider payment through non-judicial stamp paper, e-stamping, or franking, that’s you pay the duty through some franking agency or a bank that’s authorized to simply accept such a payment. Franking does involve some extra charges supported by the state you’re purchasing the property in.

Also, there are several other factors that are taken into consideration for calculating stamp duty charges. The important points are-

- Property status (new or old)

- Property area (metropolitan, rural, suburban, etc.)

- Location of property (even within a state, the charges can vary between cities and locations)

- Owner age (some states have discounts for senior citizens)

- Owner gender (some states offer a concession to female owners)

- Property usage (commercial or residential)

- Property type (independent house or flat)

The Registration Process:

While stamp duty is a fee that states charge supported the transaction value, the registration charge is the cost users pay money for the service of putting a contract or a deed in the government’s records. In simple words, the govt maintains a registry of documents in return for a fee. To an extent, this process lends inviolability to papers that may otherwise not be legally binding in nature.

The Indian Registration Act, 1908, talks about the way within which registration of documents should take place.

Stamp Duty for Women:

In order to push property ownership among women, several states charge lower duty, when a home is being registered within the name of a woman. within the national capital, for instance, women buyers pay only 4% as stamp duty in Delhi on property purchase, while the stamp duty rate is 6% for men. Lower rates are also offered, in case the home is registered jointly, with the women being the primary co-owner.

However, not all states offer this rebate to women. In Maharashtra, for instance, men and women both need to pay similar charges. the same is true of Kerala, Bihar, and Jharkhand. In UP also, women enjoy a 1% discount on it on the condition that the value of the property must not exceed Rs 10 lakhs.

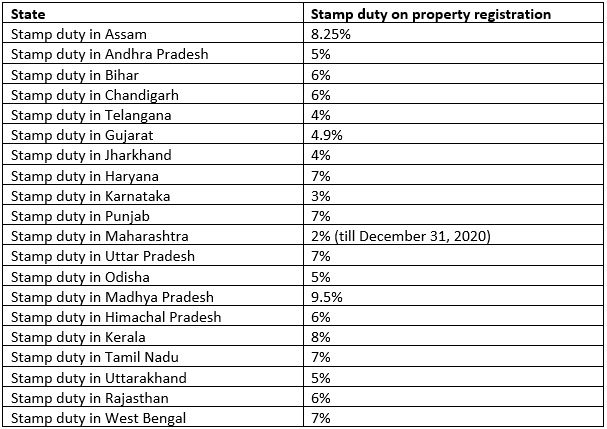

Stamp Duty in the Key Indian States:

Note: Charges mentioned in the chart are applicable to purchases in urban areas and for male buyers.

Factors Determining Stamp Duty Charges:

- Age of the Property: The age of the property plays an important role in determining the stamp duty charges you’ll be required to pay. As its charges are calculated as a percentage of the entire market price of the property, old buildings usually attract less stamp duty charges and new buildings attract a high charge. this is often because the market price of old buildings would have depreciated.

- Age of the Owner: Almost all state governments have subsidized stamp duty charges for senior citizens. So, the age of the owner plays a crucial role in determining the charge.

- Gender of the Owner: Like senior citizens, women in our country also get a reduction on stamp duty charges if the property is registered in her name. Men pay about 2% extra to get their property registration documents stamped in comparison to women.

- Purpose: Commercial buildings attract a high stamp duty fee in comparison to residential buildings. this is often mainly because commercial buildings need tons of amenities, floor space, and security measures.

- Location: If your property is found during a municipal locality or a rich populated area, be prepared to pay a high stamp tax. If your property is found in Panchayat limits or the outskirts of the town, you’ll finally end up paying less to urge it stamped.

- Amenities: Did you know that the govt will charge you for each extra amenity you’ve got on your premises while registering the property? Yes, the govt features a list of over 20 amenities that you simply will need to pay extra for if you’ve got them on your property. some of the amenities are lifts, a swimming bath, library, club, gym, community hall, and sports area.

Share this article on WhatsApp.

To apply for a home loan click here

Also read: