Home » Articles » What Are the Factors that Determines Home Loan Eligibility?

Do you want to apply for a home loan? Before you proceed to finish all the nitty-gritty, you must check your home loan eligibility. As per the eligibility of a home loan, A person must be a resident of India and should be more than 21 years of age while applying for the home loan. Depending on the bank or financial institutions where you are applying for a home loan, they need a number of documents that are required to be followed. To know more about Home Loan Eligibility, let us take a look at the various factors which determines your Home loan Eligibility:

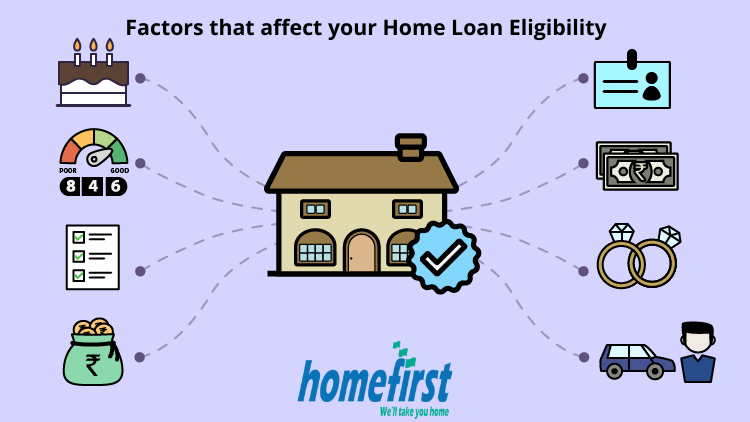

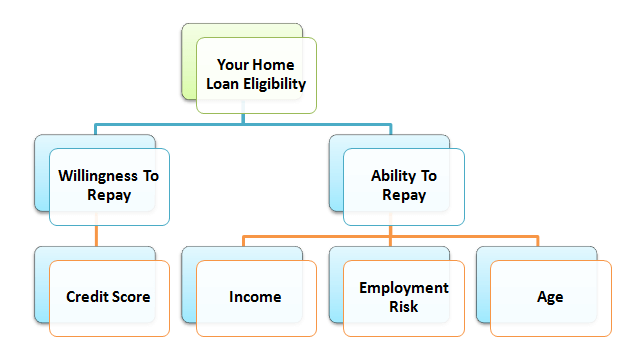

Factors Determining Home Loan Eligibility:

1. Age: Your home loan eligibility is estimated for a particular period called “tenure”. Your tenure relies on your age, and your ability to pay it off during a certain period. The ability of a young applicant to pay back his loan is different from that of a middle-aged or retired person. home loan borrowers in several phases of their lives face challenges that are very different. Banks consider such factors while evaluating applications. By planning and budgeting well, you’ll overcome the obstacles people of your age group face, and find the simplest option available to you.

2. Employment Status: Your employment status is as important as your income. Being employed in an MNC or a reputed public or private sector company makes you more reliable as a borrower. Also, if you are a self-employed individual, then lenders are more likely to offer you a sanction on flexible terms as compared to someone with an unstable job or business.

3. Income: This doesn’t require further explanation. Your income highly influences the number of money banks and financial institutions are willing to lend you. The higher your income, the greater the amount of money banks is willing to lend you. All lenders insist that applicants should have a particular level of income to be eligible for a home loan. This, of course, varies consistently with your profession. Your home loan eligibility is calculated based on your income.

4. Qualification & Experience: If your academic credentials and work experience are impressive, the chances of the bank sanctioning your home loan is higher. For instance, if you’re a salaried employee, you must have a minimum of two to three years of work experience to be eligible for a home loan. Similarly, if you’re a self-employed individual, your company must be operational for a few years, with sufficient cash profits and revenues. Tax returns must have also been filed within the company’s name. Your academic credentials and work experience predict career progress and stability fairly well.

5. Type of Employment: The type of employment will have an impression on your home loan eligibility. Banks care about whether you’re salaried, or whether you’re a Self-Employed Professional (SEP) or a Self-Employed Non-Professional (SENP). The eligibility criteria vary as per your type of employment. Frequent job changes can affect your prospects of getting a home loan.

6. Credit Score: A credit history gives a clear picture to the lender as to how you have handled your liabilities and also how capable you are of repaying the home loan. Before sanctioning the loan, lenders evaluate the credit history of the applicant, so it important to keep up a healthy credit score. Unfortunately, if you’ve got a very low credit score or many pre-existing loans, your application could also be rejected.

7. Down Payment or Margin Money: It is not merely the principal and the interest components of your EMI that you should need to worry about. You should also need to arrange the funds for margin money on the home loan. The lender funds only 80 percent of the market price of the property called (LTV) i.e. Loan-to-Value Ratio (90 percent in case of home loans below Rs 30 lakhs). The borrower must arrange the 20 percent (or 10 percent as the case may be) of the market price of the property. The down payment you’re ready to make will have an enormous impact on your home loan eligibility.

8. Market Lending Rates: The Reserve Bank of India’s (RBI) policies and market lending/interest rates have an enormous impact on your debt and advances. Interest rates determine the value of borrowing money. The higher the rate of interest, the higher is going to be the value of your home loan. In simple terms, rising lending rates will raise inflation and discourage borrowing, making savings more attractive. Declining interest rates make borrowing more attractive.

How to Calculate Your Home Loan Eligibility:

Though these parameters may vary from lender to lender and a few banks may have fewer parameters to fill in, all you would like to do is, open the calculator page and key in or select the following

- Your location

- Age or date of birth

- Select your net monthly income

- Select other income

- Select the loan tenure you’d prefer

Some banks may ask for details for the present EMIs you’re already servicing

Click on the home loan eligibility calculator to get the value of the loan you’ll expect to get.

Share this article on WhatsApp

Also read: